The second quarter of 2025 confirms a significant shift in the market that many are overlooking: the betting, casino, and slots verticals are growing, while live betting and poker are declining. We review the most relevant data from the Q2 Summary just published by the DGOJ and uncover what's behind the weakening of these two products.

The evolution of the main variables shared each quarter by the Directorate General for the Regulation of Gambling continues to show a solid and stable market, as seen from a simple reading of the main charts and figures. Furthermore, expectations remain high among operators, affiliates, and international providers who still do not consider Spain a priority market.

However, beyond the significant improvement in data such as the GGR (which increased by 18.60% compared to the same quarter in 2024), explained by growth in fixed-odds betting, casino games, and slots, we felt it necessary to take a step further and try to find the reasons behind the declines in gambling segments that now appear to be clearly deteriorating.

KEY DATA FROM Q2 2025 IN SPAIN

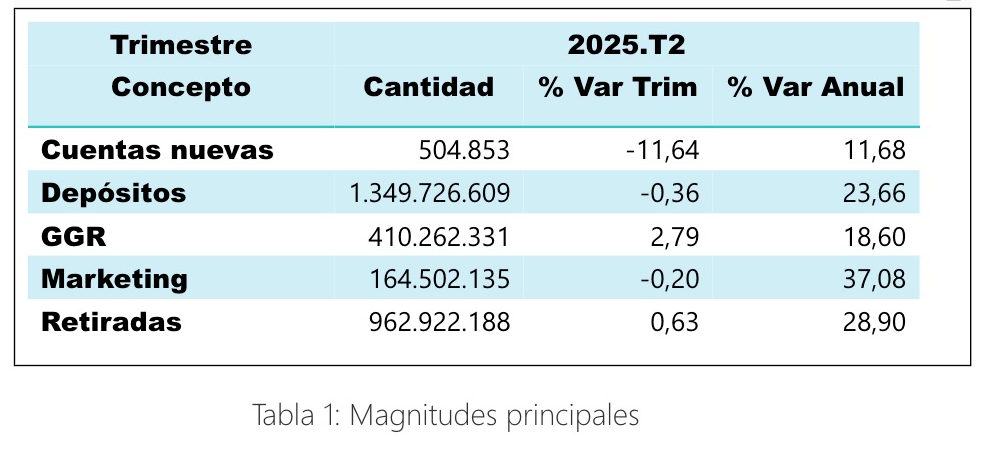

Firstly, it is worth highlighting that the total GGR (Gross Gaming Revenue) reached €410.26 million, meaning that the margin obtained by operators—after deducting bonuses and prizes—increased by +2.79% compared to the previous quarter and a notable +18.60% compared to Q2 2024.

This growth is especially commendable when analyzing the various gambling products, since in June 2024 the group stage of Euro 2024 was played, whereas in the second half of June 2025, the biggest sporting event was the FIFA Club World Cup, with matches involving Atlético de Madrid and Real Madrid in the United States. Therefore, the fact that the impact of Sports Betting on the GGR reached 41.78% remains good news for the segment in which the highest advertising investment is currently being made. Casino games (which account for 52.74% of total GGR, driven by slots, live roulette, and the rising popularity of blackjack) also continue to demonstrate that after losing relevance in 2023 and 2024, they are once again representing the largest share of gambling revenue.

In contrast, the impact of poker (4.66%) and bingo (0.82%) continues to decline considerably, consolidating a steady year-on-year drop, particularly in the second and third quarters of the year. Clearly, concerns about the future of poker operators are real, as it has been rare in the fourteen years of regulated market history to see 25% drops both quarter-on-quarter and year-on-year. Tournament poker is specifically pointed out as the most affected game type, with a -32.04% decline.

In terms of marketing and promotional activity data, promotions (bonuses) fell by 6.63% compared to the previous quarter, but grew year-on-year by +33.21%. In fact, it is estimated that bonuses released as prizes amounted to €32.70 million, while other types of promotions (not included as prizes) exceeded €49.94 million.

In any case, new accounts declined by 11.64% compared to Q1, and active accounts also dropped by 2.41% compared to the same figures published in the first quarter.

- Within betting licenses, there are mixed results: while "fixed-odds sports betting" increased by +24.55% (compared to the previous quarter), live betting dropped a surprising 33.24%.As for casino licenses, there was a global growth of +6.53% compared to Q1 2025 and a commendable +25.98% year-on-year, with slot machines up +33.58%, accompanied by a significant rebound in blackjack and the consolidation of live roulette as the sector’s star product.

- In terms of marketing and promotional activity data, promotions (bonuses) fell by 6.63% compared to the previous quarter, but grew year-on-year by +33.21%. In fact, it is estimated that bonuses released as prizes amounted to €32.70 million, while other types of promotions (not included as prizes) exceeded €49.94 million.

In any case, new accounts declined by 11.64% compared to Q1, and active accounts also dropped by 2.41% compared to the same figures published in the first quarter.

Operators continue to invest

Supported by the new scenario brought about by the Supreme Court ruling and the absence of warnings or sanctions regarding the increasing use of influencers and well-known personalities, marketing expenditure continues to grow and now exceeds €164.50 million. This amount benefits major media groups, Google and social media platforms, agencies, and affiliates with a presence in Spain. The figure is broken down as follows:

- €82.64 million in promotions

- €62.91 million in advertising

- €13.99 million in affiliation

- €4.96 million in sponsorship

Compared to the previous quarter, there is a significant increase in sponsorship (+52.98%) and advertising (+5.37%), while promotions decreased by -6.63%. Year-on-year, the figures are even more striking, with sponsorship growing by 311.92%, advertising by 42.96%, promotions by 33.21%, and affiliation by 9.64%.

These figures leave no room for doubt: Spain is seen as a market where investing in visibility is worthwhile, especially through sports sponsorship, confirming operators' commitment to making their brands known to the general public.

Explaining the decline in Live Betting

The 33.24% drop in live betting compared to Q1 2025 is substantial, especially considering that “conventional fixed-odds betting” rose sharply (+24.55%) during the same period. This shows that something is driving players away from what happens “live.” Based on consultations with several operators and affiliates, the following hypotheses stand out:

1)

On the technological front, the user experience in live betting depends almost entirely on update speed and platform stability. Delays in odds updates, freezes during key moments (penalties, corner kicks, break points in tennis), or constant market suspensions cause frustration and erode player trust. It is a fact that several of the most relevant betting operators in Spain have yet to improve the live user experience.

2)

From a behavioral perspective, the growth of pre-match betting and the decline in live betting also reflect a shift in bettor profiles. This is evident in the behavior of tipsters and the explicit betting content promoted by operators, which tend to recommend planning bets in advance, analyzing calmly, and avoiding the pressure of the immediacy that live betting demands.

3)

Risk management strategies by betting companies are increasingly giving less visibility to live betting—a product that is harder to model, exposes operators to greater losses in case of trading errors, and can give an edge to expert bettors using automated systems. It is noteworthy how many operators have reduced the depth and variety of live markets, focusing their commercial incentives on pre-match bets.

4) Some affiliates (especially those focused on odds comparison) also point out that

the rise of promotions such as “offers for wins by more than 2 goals,” “scoring substitutes,” and especially boosted odds and all promotions related to accumulator bets, is leading players to focus on pre-match markets, which are far more attractive in terms of potential extra winnings.

5) As seen in the same report,

new accounts dropped significantly by 11.64% compared to Q1, suggesting a lower recent influx of players. Therefore, given the reduced competitiveness of live betting odds, seasoned bettors tend to prefer pre-match odds, which are generally higher.

The drastic decline of poker

Despite the fact that operators like Winamax continue to offer online tournament series with guaranteed prizes approaching €20 million in just ten days of events (in Q3 2025, the Winamax Series guaranteed €19 million), or that PokerStars continues to host live poker festivals breaking participation records, the decline in traffic on online poker rooms has become more pronounced, as confirmed in this Q2 2025 report by a sharp decrease in poker’s share of GGR.

And this is the case even though marketing spend remains stable, and has even increased in terms of audiovisual productions featuring well-known influencers participating in poker games streamed on major platforms like YouTube, Twitch, or Kick (such as 888poker’s

Noche de Poker, PokerStars’

Poker Night, or Winamax’s

La Timba).

But the main reason behind this poker downturn is a strategic one: with the exception of Winamax (which does not hold a casino license), poker is increasingly becoming a product aimed at channeling its players toward more profitable verticals for the operator. Thus, new users entering a regulated operator’s poker tables often receive cross-sell incentives and promotions designed to push them toward casino or sports betting.

We can observe this trend at

Sportium,

PokerStars,

Bet365,

Betfair, or

888Poker, where poker-specific promotional incentives are becoming increasingly rare, or where such promotions are being reallocated to other products like casino games.

In our 2024 article on Infoplay titled “

Cross-selling in Online Gambling Marketing,” these findings were already anticipated by explaining how cross-selling is transforming the reality of the Spanish online market—boosting player activity and showing that operators with multiple verticals (casino, poker, betting) are using this strategy to retain existing users and motivate them to try other types of games.

CONCLUSION

The in-depth analysis of the

Summary for the Second Quarter of 2025 shows that the overall evolution of the main indicators related to operator performance and player preferences continues along the usual positive trend that has characterized the sector since the Supreme Court annulled a significant portion of the online gambling and betting advertising law. However, we believe it is important that these results not be interpreted solely from a general numerical perspective, but rather that the underlying circumstances behind certain notable declines—such as in online poker and live betting—should be properly understood.

18+ | Juegoseguro.es – Jugarbien.es

: Live betting and poker collapse")